Retailer supporting information - lines charge changes for the 1 April 2023 to 31 March 2024 pricing year

This page is intended for retailers and assumes readers have a good level of distribution pricing knowledge

Price decreases for residential customers, and price increases for some commercial customer from 1 April 2023.

Our Price Setting Compliance Statement, Pricing Methodology and Pricing Roadmap disclosures provide the methods and processes we have used to calculate this year’s prices. The disclosures also provide an overview of the reasons for price changes. We will be releasing these disclosures early March 2023 in line with our regulatory requirements.

The purpose of this update is to provide an overview of this year’s price changes to support the release of tariffs which are provided before our regulatory disclosures are made public.

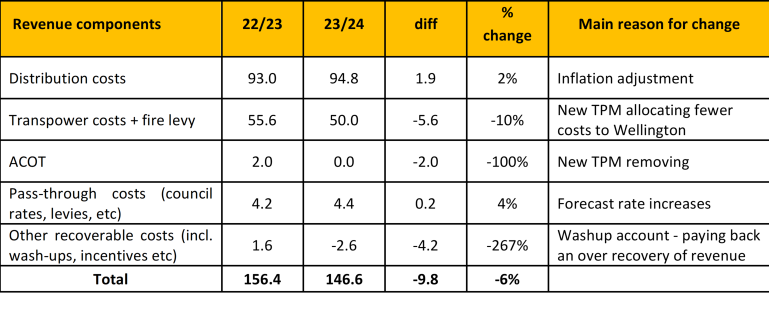

We set our tariffs based on the revenue that the regulatory framework sets for us to collect. Revenue to be collected from prices has decreased by 6%. The key drivers of the decrease in revenue are provided in the table below.

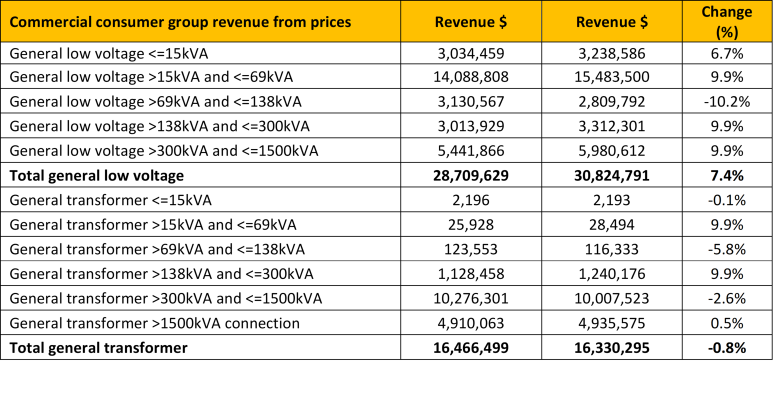

While overall revenue and therefore prices have decreased, wider price reform means that there are different price changes between residential and commercial prices. The application of the Electricity Authority’s new methodology for calculating and allocating Transmission costs, and the second year of the governments phasing out of low fixed tariffs restrictions has decreased lines charge for residential consumers by an average of 8% for low energy users and 13% for standard users. Commercial customers’ prices will increase on average by 10% for some price categories and decrease for others. The tables below provide the change in revenue for each customer group.

Impact of volume changes

Prices have fixed and variable components, each requiring separate quantity forecasts – the fixed component requiring a forecast for the number of new connections and the variable component requiring a forecast of volume (kWh).

We are forecasting an increase in the number of new connections and an increase in energy used for residential customers. Our forecasts include an increase in electric vehicle volumes and an increase in the number of people working from home post covid-19. The increases mean that actual price increases will be on average 1% less than the decrease in revenue provided above. Higher volumes means that revenue is collected over more customers and units of energy used, so the unit prices are less. The 1% increase in volumes is an average – the actual impact will vary between price categories.

Large increases in fixed tariffs and decreases in variable tariffs

Customer prices have a fixed and variable component. The fixed component doesn’t change with energy use and is either a daily fixed charge or a capacity charge. The variable component varies with energy used (kWh), any time peak demand (kW), peak demand (kW) or energy used during peak and off-peak time periods (kWh).

The application of the Transmission Pricing Methodology (TPM) to an EDB’s share of Transmission costs, and the transition away from the Low Fixed User restrictions means there is a shift from variable tariffs to fixed tariffs. This means the overall amount of revenue collected from fixed prices will increase and the amount from variable prices will decrease. This year’s tariff changes include large offsetting changes between these two tariff types. The overall price change a customer will see will depend on the offsetting amount between the tariff types. For example, the Residential Standard User Uncontrolled daily tariff has increased from 99c to $1.2 (a 24% increase) and the Standard User Uncontrolled variable tariff has decreased by 44%. The overall impact is a 13% decrease.

Application of the TPM to Transmission cost

The largest driver of this year’s price changes is the application of the Electricity Authority’s TPM to the Transmission costs that have been allocated to the Wellington network. In November 2022, we provided a pricing note detailing how we will be applying the TPM to Transmission costs and the forecast customer impact. Several customers provided feedback which we responded to in January 2023. These documents and other pricing files are provided at the bottom of this page. In summary, the key changes and pricing impact are:

- Changes in the overall costs assigned to each distribution network to pass through. Transmission costs assigned to Wellington Electricity (including the removal of ACOT) have decreased by $7.6m or 13%.

- Change in the cost allocation methodology used to pass through costs to customers. Costs will all be passed through as a fixed tariff (the exception being residential prices which still have low fixed user restrictions). The change in allocation methodology also means that more revenue will be allocated to commercial customers and less to residential customers. This reflects a shift from using peak network demand to allocate transmission costs, to using energy used and connected capacity.

The pricing note and feedback response letter provides more detail about these changes.

Second year for the Low Fixed User Transmission

The legislation that restricts the size of the fixed price component for low electricity users (less than 8,000 kWh per year) is being removed over a five-year period. The Electricity Authority has also now confirmed their expectation that EDBs will remove Low Fixed User restrictions.

We are in the second year of the transition – fixed prices for low users have increase from 30 cents per day to 45 cents. Overall, the change has resulted in a 2% price change between low user (increased by 2%) and standard user tariffs (decreased by 2%).

Consultation on Distribution price structure changes

In November 2022, we also consulted on a future price structure for Distribution price. We are not planning to start the transition to these price structures until 2024. The consultation included:

- Proposing a distribution pricing structure that reflects the Authority’s new pricing methodology and Pricing Principles. The proposed structure also simplifies our pricing structures.

- Consulting on transition rules to guide how we move from existing price structures to the proposed future price structures.

The consultation is included in the Pricing Note at the bottom of this page. Thank you for those who provided feedback. We will be providing a response shortly. We also noted during the consultation that we need to do more thinking about price structures for large commercial customers. We plan to consult again this year.

Related Documents

Consultation:WE TMP Price Changes and Future Distribution Prices

Consultation document for Retailers from November 2022.

1.4 MB | pdf

Response to Retailer Questions: TMP Consultation November 2022

Response to Retailer Questions: TMP Residual Pricing Approach Consultation

153 KB | pdf

WE 1 April 2023 Pricing Schedule

Printable version of Wellington Electricity's 1 April 2023 pricing, for retailers.

21 KB | xlsx

CKHK EIEP12 File

Wellington Electricity pricing for the pricing year starting 1 April 2023 in the industry prescribed EIEP12 file format.

17 KB | xlsx

To help improve our service, what feedback can you give us about this page?